That’s an amazing concept to me. I grew up fascinated – and to a degree entranced – by the concept of consumer credit. But my Dad would have had me out to the woodshed if he even thought I’d tried to ‘finance’ Fast Food purchases…

‘Nola’ of The Nola Grind describes himself as, “a professional poker player

[who] also grinds DoorDash, UberEats, Grubhub, and catering apps…”

This issue doesn’t sound like such a biggie, in the context of the debt-ridden, half-underwater ex-istence many ordinary folks are living today. But I contend it’s actually a major watershed in the future of ‘personal finance’, as well as huge ‘gimme’ to Fast Food purveyors.

Its most dangerous feature may be how easy it makes it fall even deeper into debt without even realizing it… Klarna and services like it may well prove to be a financial last straw from which millions of folks – mainly younger ones – will never be able to get out from under.

Tempting ‘transparency’

Many younger people today – especially those out in the working world and responsible for their own money – are already facing the realization that they may never get out from under their per-sonal debt load. Much less be able to save enough to finance any kind of retirement.

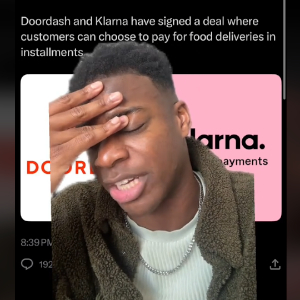

Now, though – as if to rub that in – a finance company I’d never heard until this morning is making it possible for Fast Food fans to ‘afford’ the rising cost of their fix by arranging ‘on the spot loans’ for cash-strapped FF junkies.

Enter, Klarna…

Klarna is a Swedish company specializing in fully-integrated financing of small-dollar purchases such as Fats Food orders placed digitally and delivered by services such as Door Dash.

“Klarna is the smooothest way to get what you want today and pay for it over time,” its official wesite schmooses. “Split your purchase into 4 payments, and avoid fees when you pay on time.”

But everything about Klarna strikes me as an insidious new way to pick the consumer’s pocket.

The deal features, “the simplest one-time sign-up process you’ve ever used.” And, “require[s] only basic information at the checkout, so you can complete your purchase with full transparency.”

The first payment is made at the checkout and the remaining payments are automatically collected every 2 weeks, “so you don’t have to lift a finger…”

Social media up in arms

Legions of online commenters agree with me, warning the Klarna plan is sheer madness. Influencer Farai Bennet (pictured left) simply calls it, “bizarre!”

Legions of online commenters agree with me, warning the Klarna plan is sheer madness. Influencer Farai Bennet (pictured left) simply calls it, “bizarre!”

“If you have to finance your burrito bowl, it doesn’t scream golden age of prosperity.” Internet personality Matt Buechele shared. “If you have a four-installment payment plan for a McFlurry, you’ve lost the plot, my friend.”

“Never thought it would get to financing fast food,” another social media commenter observed.

“This can’t be real life 🤦🏽♀️😫,” sputtered a fourth…

My take

What really got me was a notation on the Klarna wesbite – repeated in other online stories and references to the service – that this deal isn’t conventional credit: it’s just a friendly ‘buy now, pay later’ plan. That’s what they called the original consumer credit programs.

Some Boomers may be old enough to recall other euphemisms such as ‘time payments’, and ‘installment plans’. They’ve been tempting (and tormenting) consumers since before credit cards existed. There’s truly ‘nothing new under the sun’.

(And I’m going to resist making any sort of sarcastic reference to ‘newstalgia’, in this context!)

~ Maggie J.